Coin Alpha: January 2021 Outlook

"Markets beat hierarchies when sourcing information about the future." - Fred Ehrsam

Going Parabolic

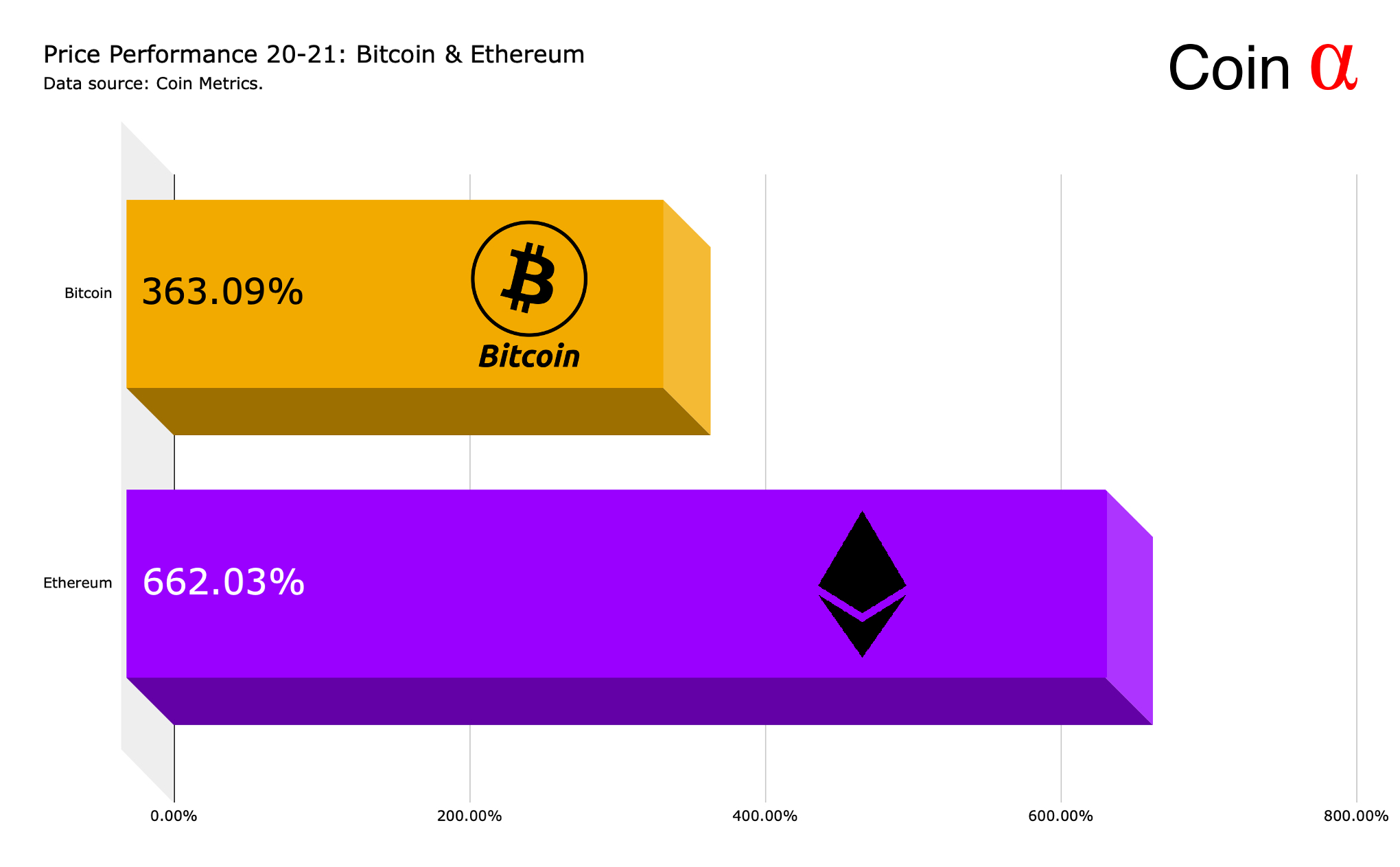

Digital assets are currently presenting parabolic growth, surpassing all expectations. Bitcoin (BTC) acts as a leading indicator to the market and pulls other premium assets, i.a. Ethereum (ETH), into its vortex. Bitcoin has incrementally been supported by institutional demand (GBTC, MSTR) since 2020 and looks stronger than ever before. However when observing early 2021 price data, Ethereum has grown even more (662,03 percent) in 20-21, using bitcoin (363,09%) as a benchmark.

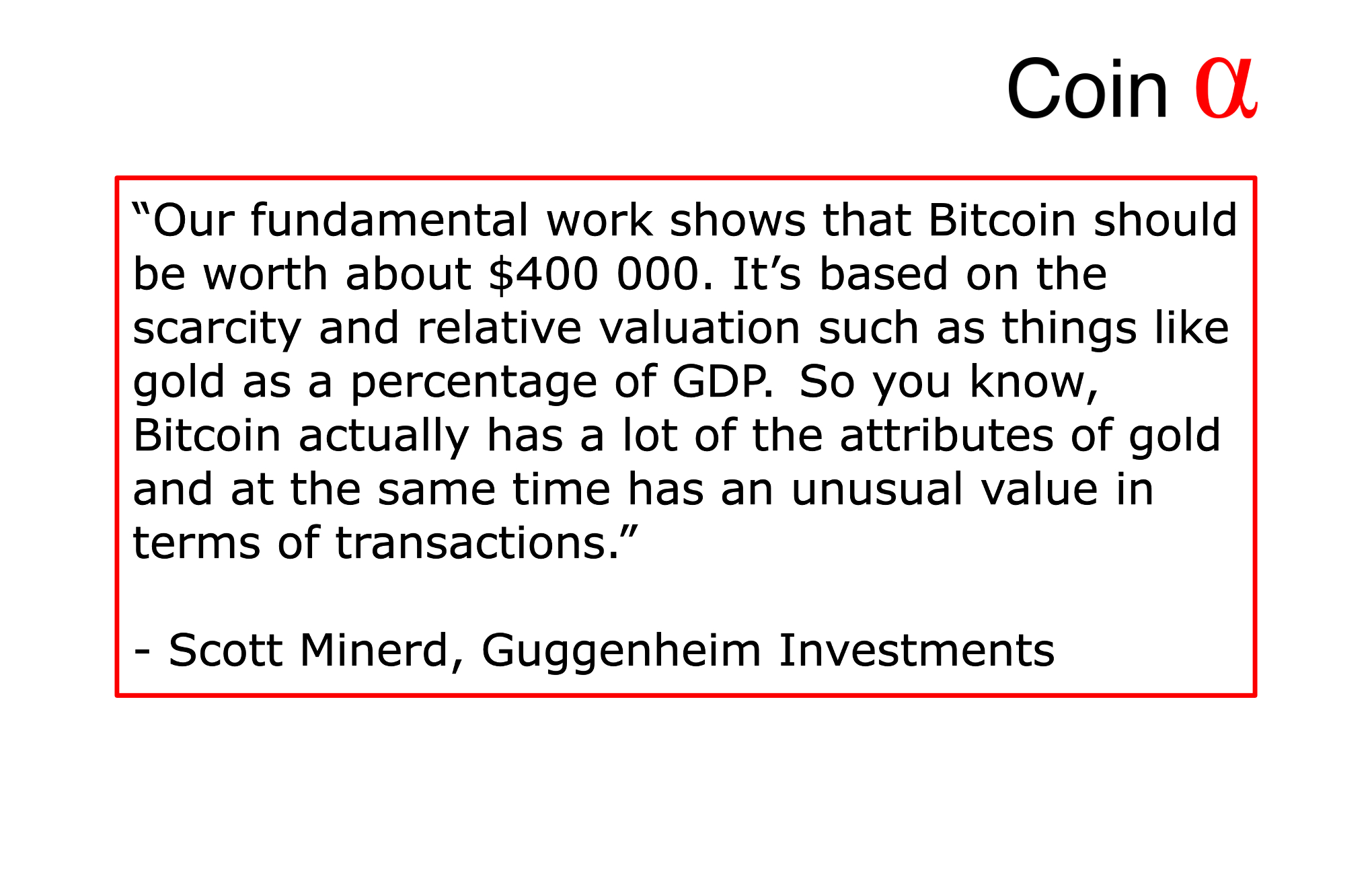

The inherent question seems to be: How high can bitcoin’s price go? Guggenheim Investments proposes a 400 000 USD valuation for each bitcoin, based on bitcoin’s scarcity and relative valuation compared to gold. One simple, yet effective, calculation would be dividing the global supply of money (5 trillion dollars) by bitcoin’s circulating supply (18,59 million). 5 trillion ÷ 18,59 million = 268 961,81 dollars. This estimation would be relatively close to numbers proposed by institutions like Guggenheim and ARK.

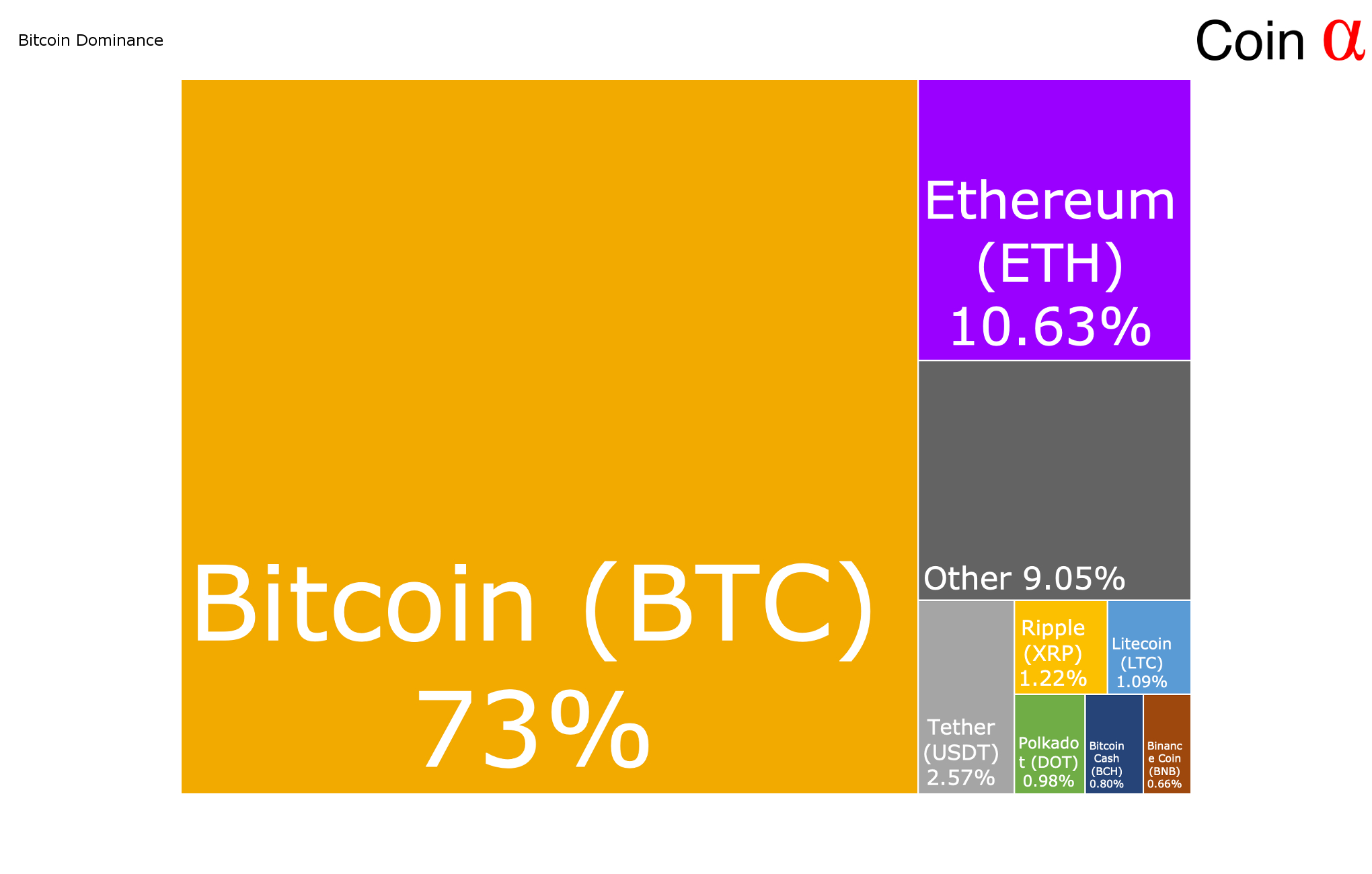

Furthermore bitcoin has been increasing its relative dominance, currently at 74 percent. Ethereum comes as second with 10,63%. Some smaller digital assets like Polkadot (DOT) have been increasing their market cap (0,98%). As an Ethereum rival, Polkadot maintains a ecosystem for new decentralized economy.

While bitcoin “dominance” compares market cap data, MCAP is only a relevant metric when it’s supported by volume relative to MCAP, and when volume comes from a broad group of participants that are representative of market demand. Many altcoins don’t fit the criteria above, so the real (organic) bitcoin dominance is likely well above the indicated percent.

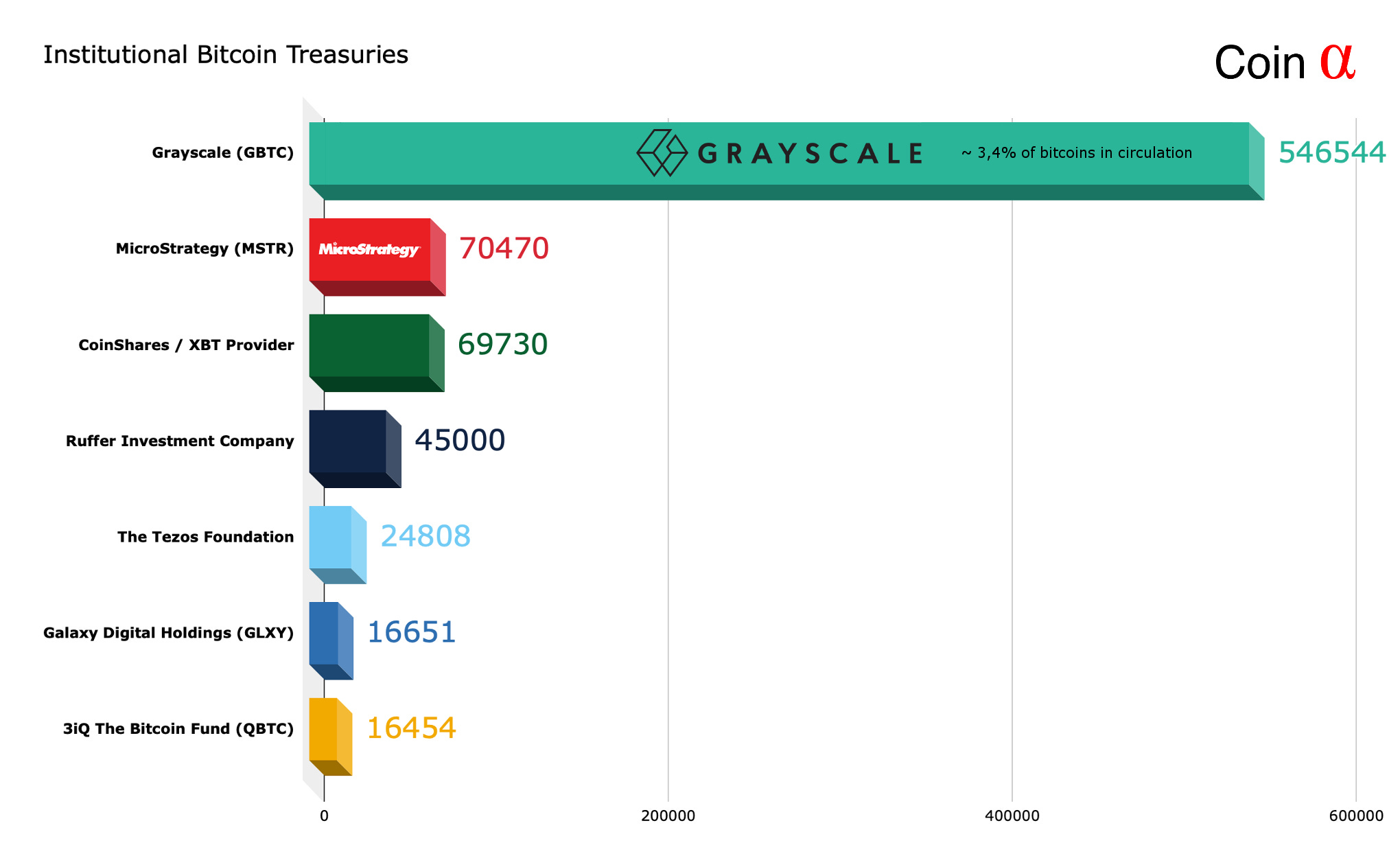

Institutional Adoption

“Money is flowing out of conventional assets into Bitcoin due to the escalating risks of global currency devaluation, technology disruption, social dislocation & political uncertainty. This is not a “rally” or “bubble” - it’s a chain reaction spreading like a fire in cyberspace.” - Michael Saylor, MicroStrategy

The current market cycle, emerging in 2020, has been characterized by growing institutional demand. Perhaps the most famous Bitcoin allocation was made by MicroStrategy (MSTR), an US-based business intelligence company. MicroStrategy’s CEO Michael Saylor has distinctively positioned himself as a “bitcoiner”, allocating his own wealth vis-à-vis MicroStrategy’s resources. Saylor sees Bitcoin as “hard money” and store of value (SoV). Additionally he’s mainly indicating using Bitcoin as an instrument to hedge global currency devaluation, technology disruption, social dislocation & political uncertainty.

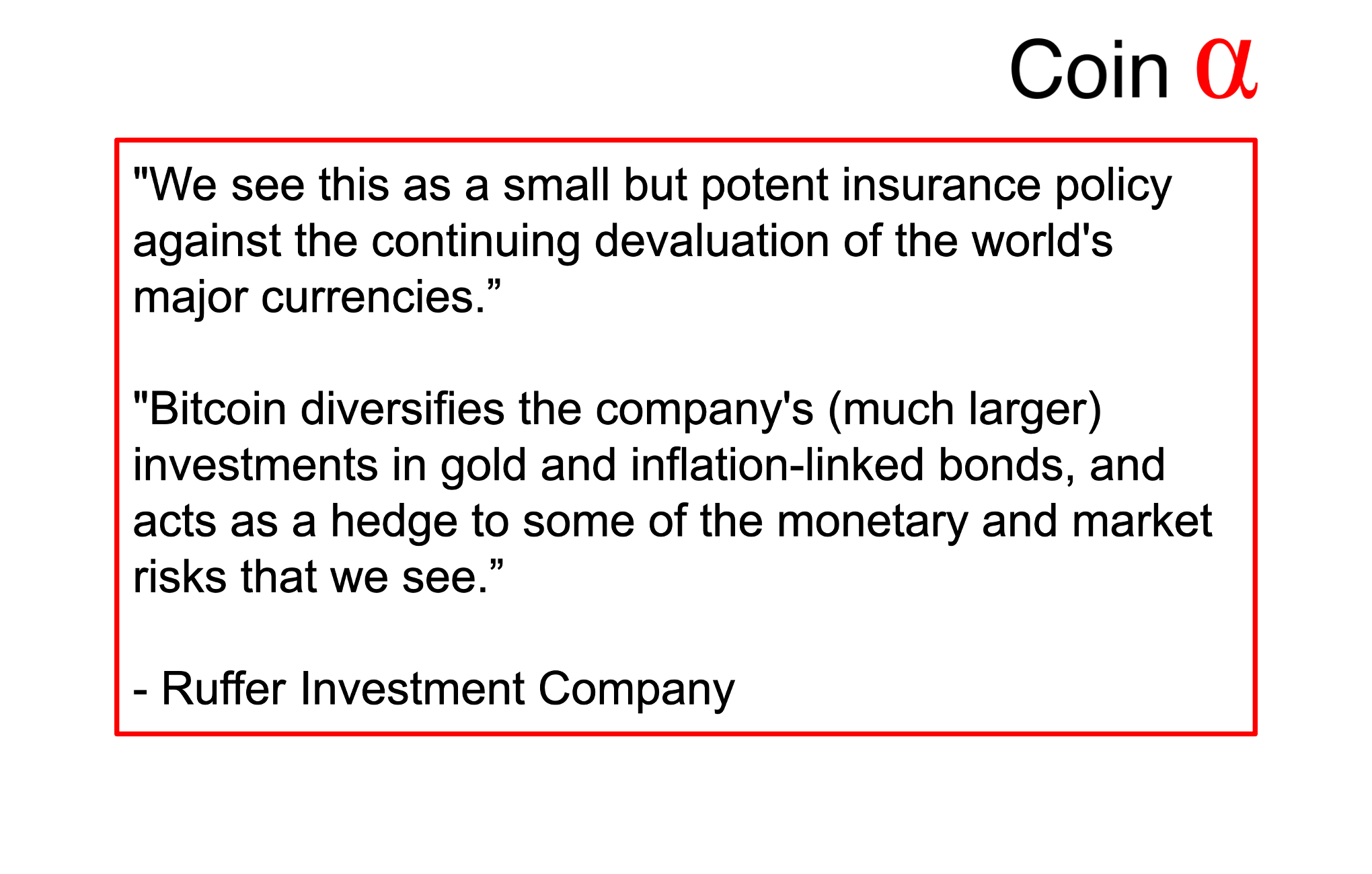

In addition to MicroStrategy’s huge allocations, companies like Guggenheim Partners and Ruffer Investment Company are entering the space. Guggenheim Partners has reserved the right to set aside as much as 10 percent from its $5,3 billion Macro Opportunities Fund to invest in Grayscale Bitcoin Trust (GBTC). Ruffer Investments Company allocated 2,5% of its $20 billion portfolio into Bitcoin in November 2020.

Besides to all institutions mentioned above, VanEck Assosiates Corp. has filed an application for Bitcoin ETF, according to SEC. Bitcoin ETF would possibly become reality during 2021.

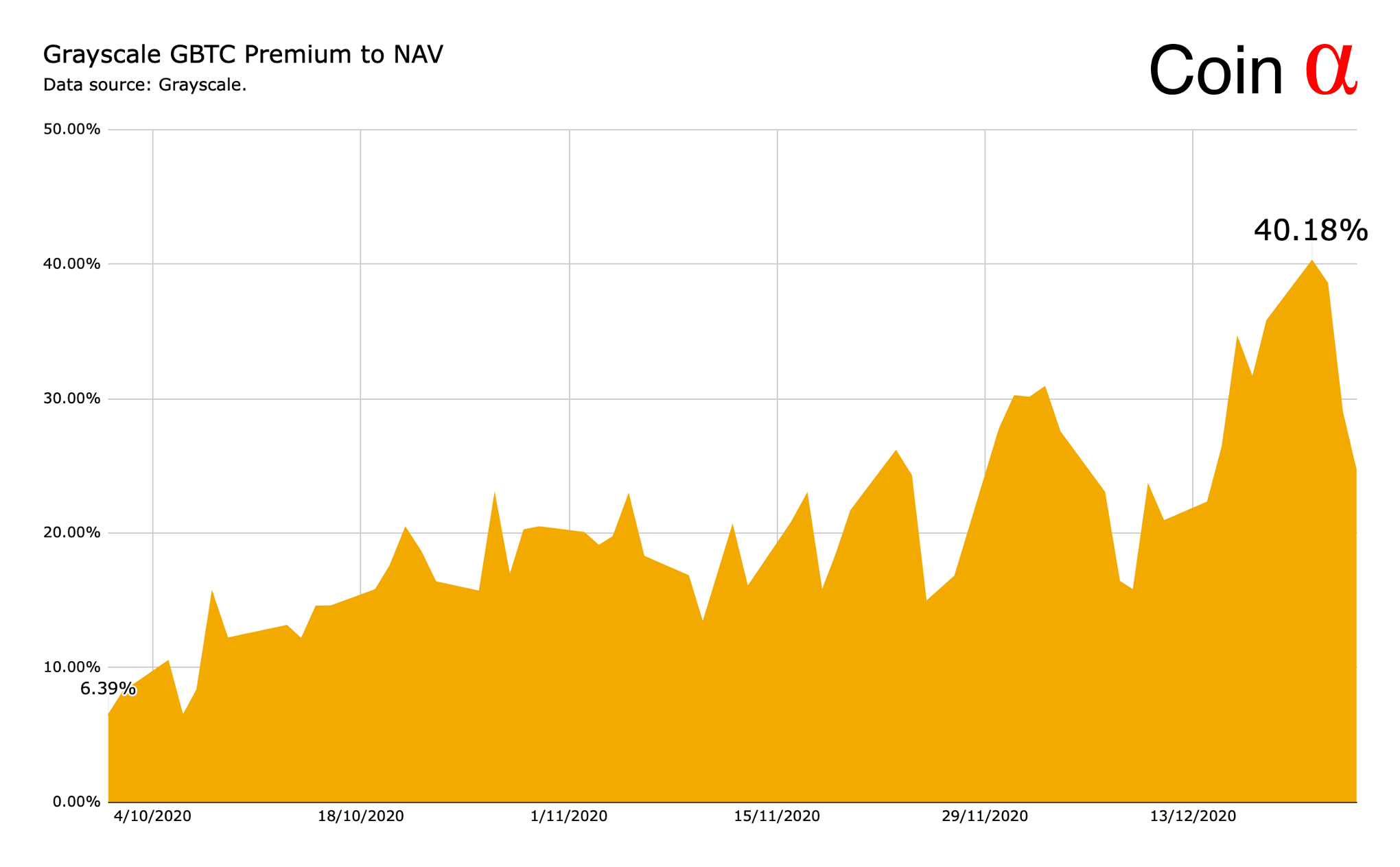

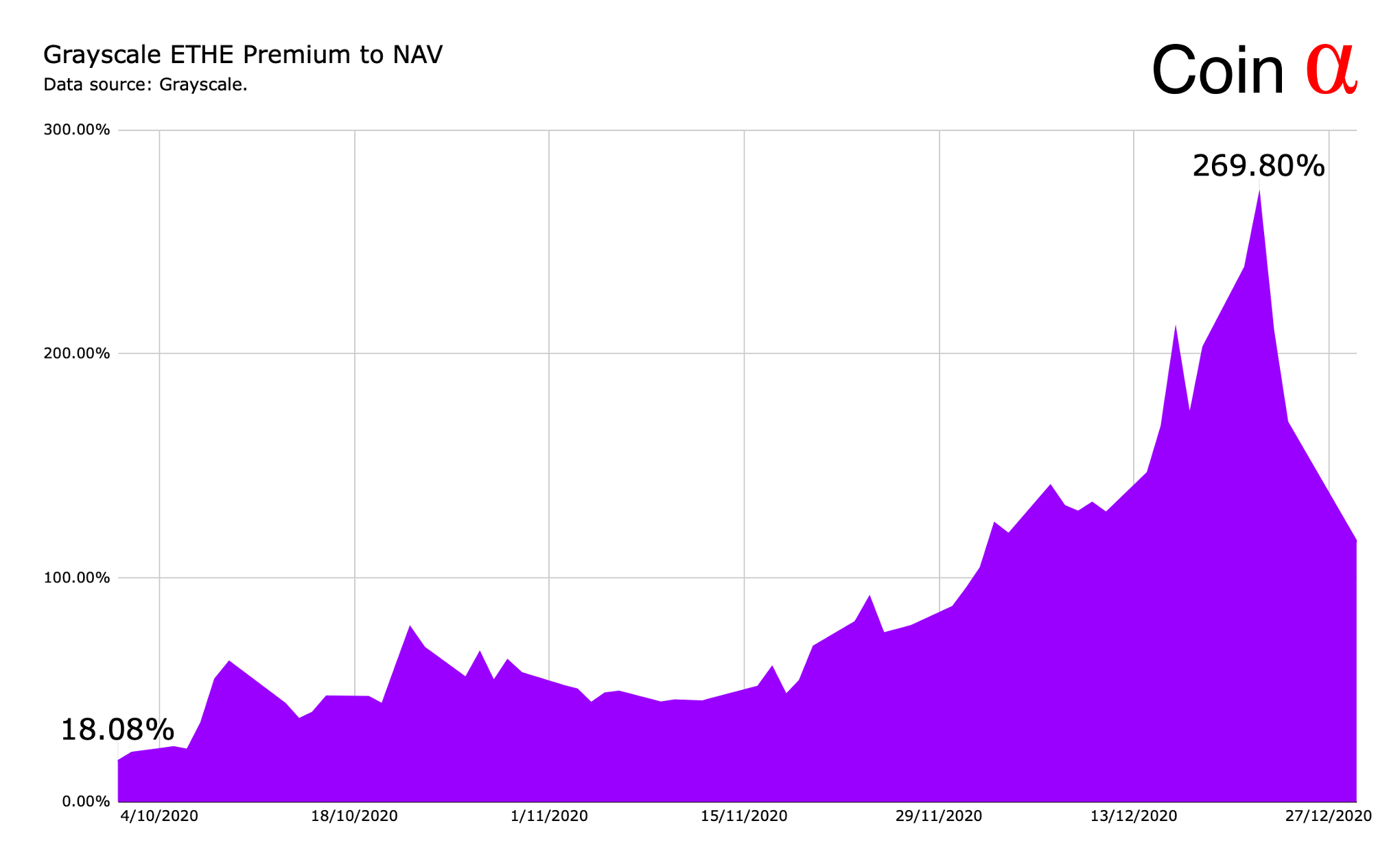

Grayscale Premiums Up

Grayscale premiums for Bitcoin Trust (GBTC) and Ethereum Trust (ETHE) have been increasing since early Q4 of 2020. GBTC’s premium peaked at 40,18 percent in late December 2020 and ETHE’s at 269,80% during the same timeframe. The increasing GBTC and ETHE premiums mirror growing demand for digital assets, Grayscale’s client portfolio mainly consists of institutional investors.

Bullish (overbought) sentiment = Divergence between NAV and premium. Increasing premium.

Bearish (oversold) sentiment = Convergence between NAV and premium. Decreasing premium.

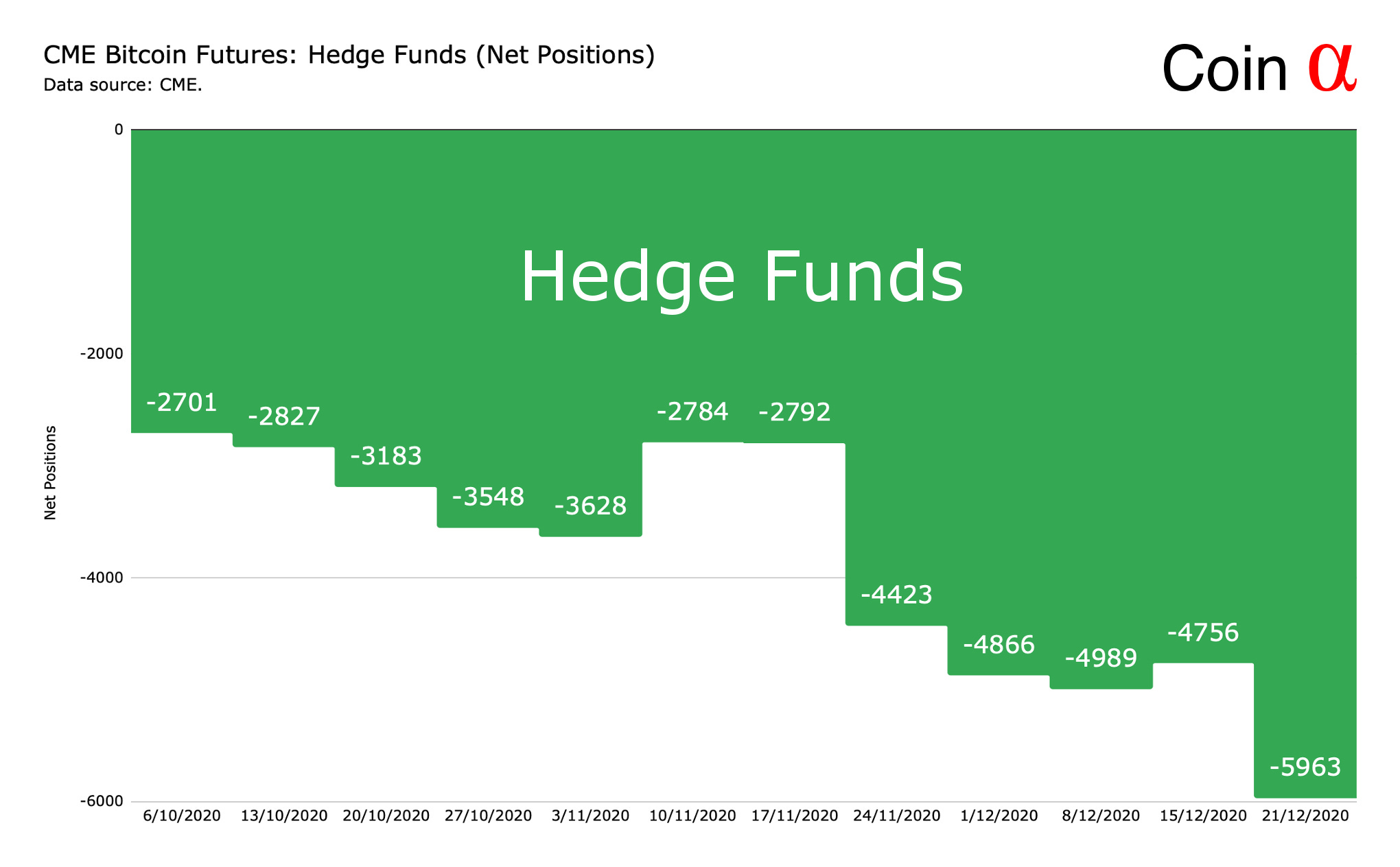

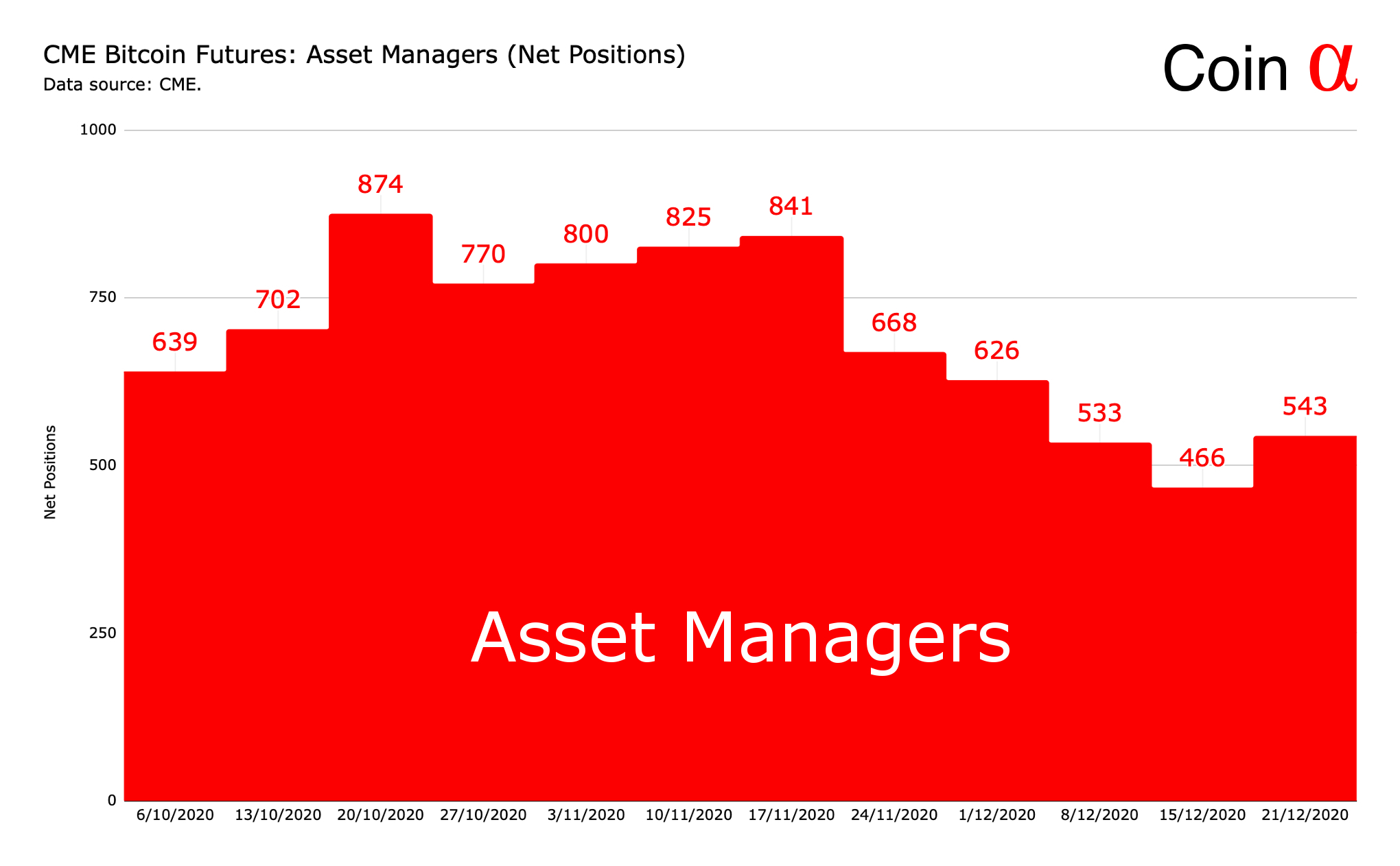

COT Analysis for CME Bitcoin Futures

Bitcoin Futures by CME are one of the oldest bitcoin-related financial products, launched in late 2017. CME Bitcoin Futures volume has been increasing correlated with bitcoin’s price, rising above 2 billion dollars in late 2020.

Retail investors are holding an increasingly bullish attitude towards bitcoin with an average of 2667 net positions during the fourth quarter of 2020. Bitcoin’s 2020 cycle has been supported by institutions, COT data might suggest deferred but growing retail interest.

Hedge funds have historically been bearish on bitcoin and COT data supports this hypothesis. Hedge funds held -3872 net positions during fourth quarter of 2020. However the digital asset market is not fundamentally driven by derivatives. Institutional buyers are mainly accumulating through the OTC market which is even larger than exchanges combined.

Asset managers held 691 net positions on average during fourth quarter of 2020. By increasing demand, asset managers have pivoted more and more into digital asset. From a historical perspective, even 1-5 percent allocation in bitcoin has significantly boosted portfolio performance.

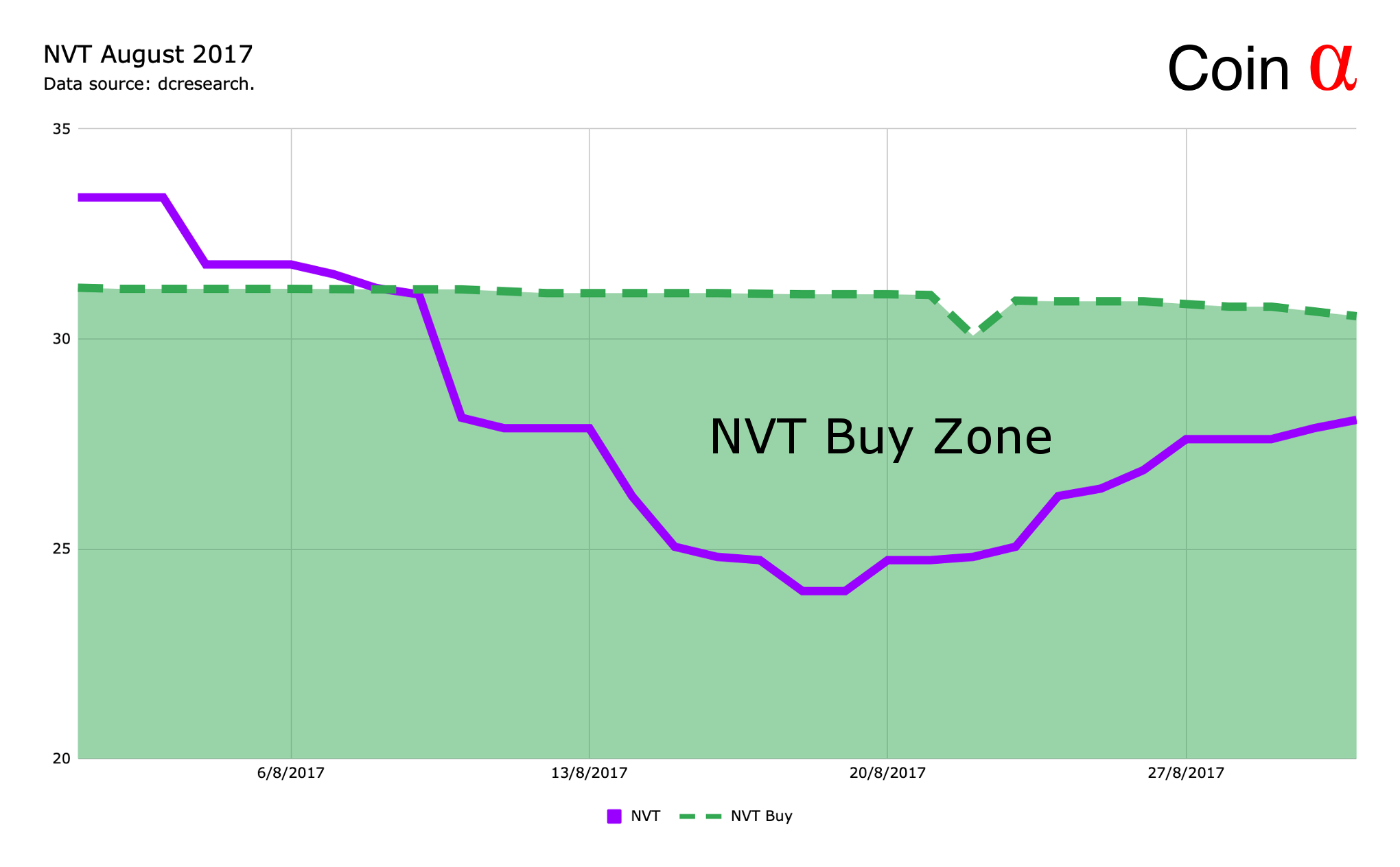

Bitcoin Bouncing on NVT Buy Zone

Bitcoin NVT is calculated by dividing the Network Value (MCAP) by the the daily USD volume transmitted through the blockchain. NVT is a core instrument for indicating whether bitcoin’s price is overvalued or undervalued.

Bitcoin NVT has been bouncing on NVT buy zone from fourth quarter of 2020 onwards, indicating a clear opportunity to enter the market. Bitcoin NVT also dived into the buy zone during November, mirroring bitcoin undervaluation. During November’s dive into NVT buy zone bitcoin’s price was approximately $15K, therefore it has doubled since.

NVT has been a crucial indicator before, during token-induced rally of 2017, bitcoin took a deep dive into NVT buy zone. In August 2017 bitcoin’s price was approximately $4K, incrementally rising into $19K later that year.

Want to Know More?

Subscribe to Coin Alpha’s future updates here on Substack.

Editor: Timo Oinonen. LinkedIn. Twitter.

Disclosure: The information provided is for informational purposes only and is subject to change without notice. The information presented in Coin Alpha should not be construed as investment advice.