Coin Alpha: December 2020 Outlook

“If you can produce more of it with labor, capital, & technology, it’s a commodity. If it’s unique, irreplaceable, and brings you joy, it’s a scarcity. Sell commodities so you can buy scarcities.” - Michael Saylor

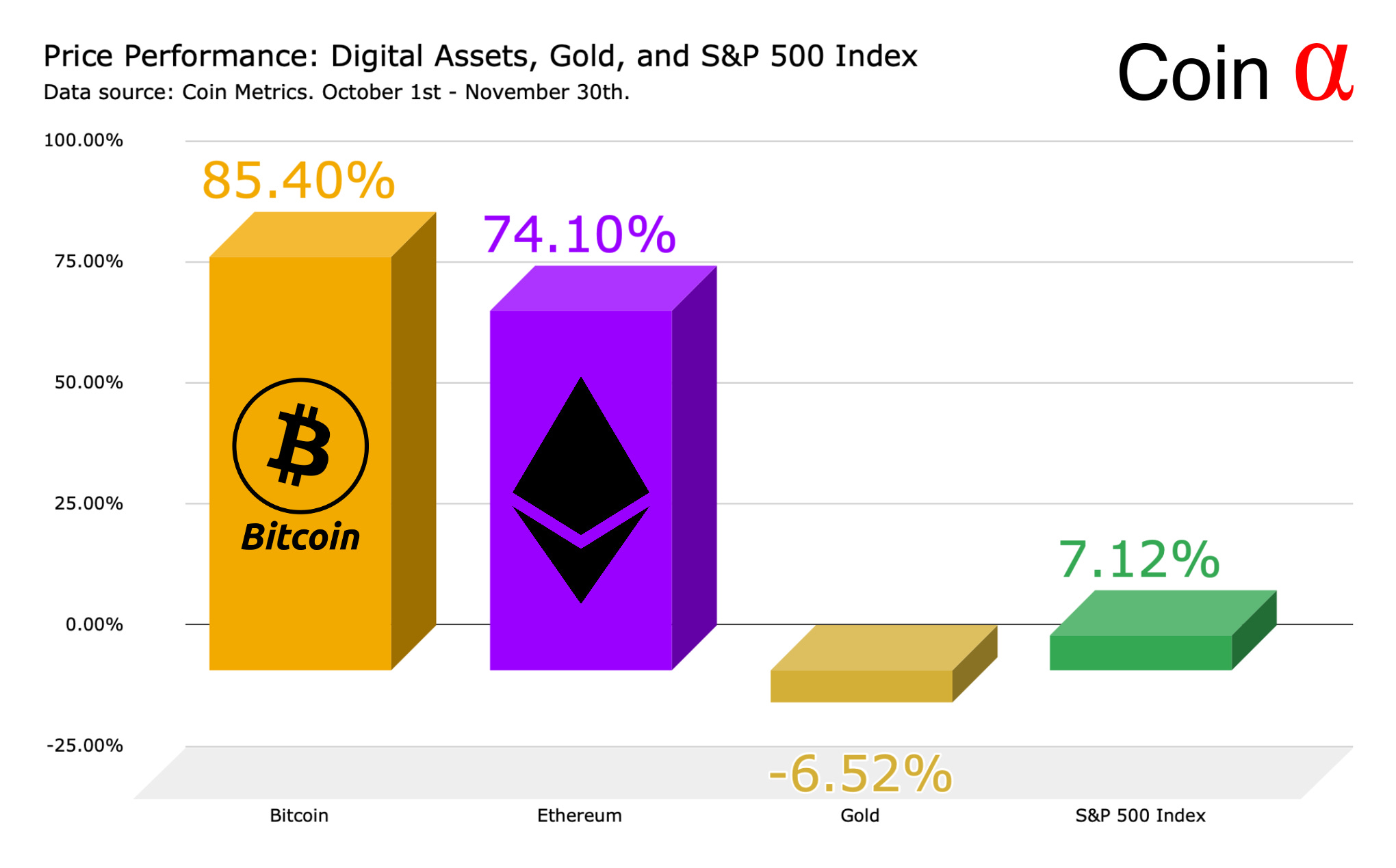

Bitcoin Decoupling from Gold, High Correlation with Ethereum

Bitcoin (BTC) maintained its sovereignty over other asset classes, rising 85,4 percent from early October to late November. Bitcoin’s momentum also benefited Ethereum (ETH) notably, as the heavily correlated digital asset rose 74,1% during the same time frame. Bitcoin and Ethereum have historically been in tight correlation.

Gold (XAU) showcased substandard performance during the same time frame, dropping -6,52%. Bitcoin has clearly decoupled from the benchmark “store of value” asset gold and one could even argue that gold’s narrative as the de facto safe haven has been broken, at least temporarily. Stocks (S&P 500 Index) performed satisfactorily, rising 7,12% in the heavily stimulated market.

Bitcoin Liquidity Increasing, Driven by Institutional Growth

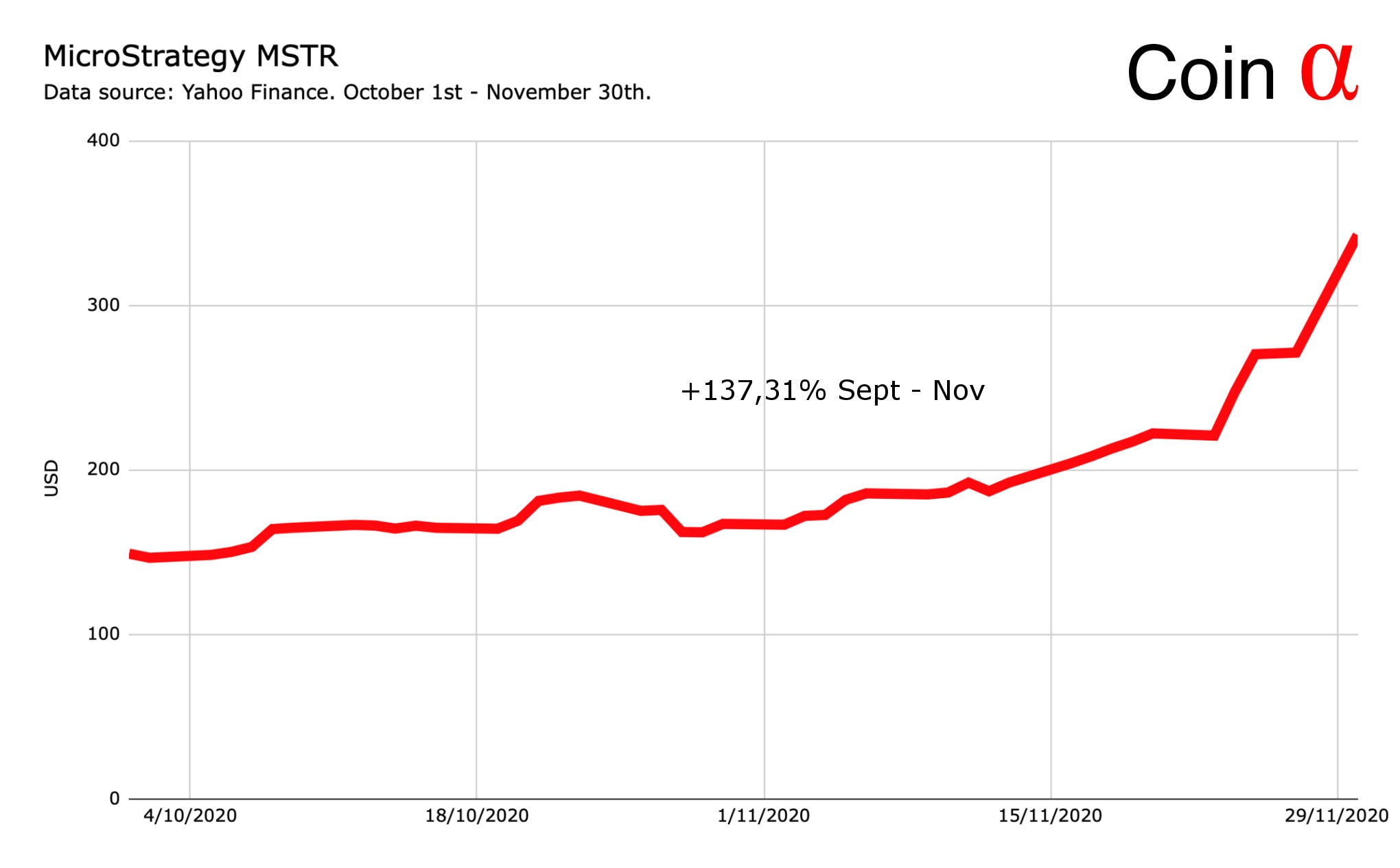

Coinbase, one of the leading cryptocurrency exchanges globally, executed MicroStrategy’s (MSTR) 425 million dollar bitcoin (BTC) purchase in September. The purchase was implemented in multiple phases during approximately 5 days and there was no significant movement in the market. MicroStrategy’s recent purchase mirrors bitcoin’s established liquidity, a relevant attribute for institutional investors entering the market.

MicroStrategy’s allocation into bitcoin clearly boosted MSTR stock, rising 137,31 percent from September to November.

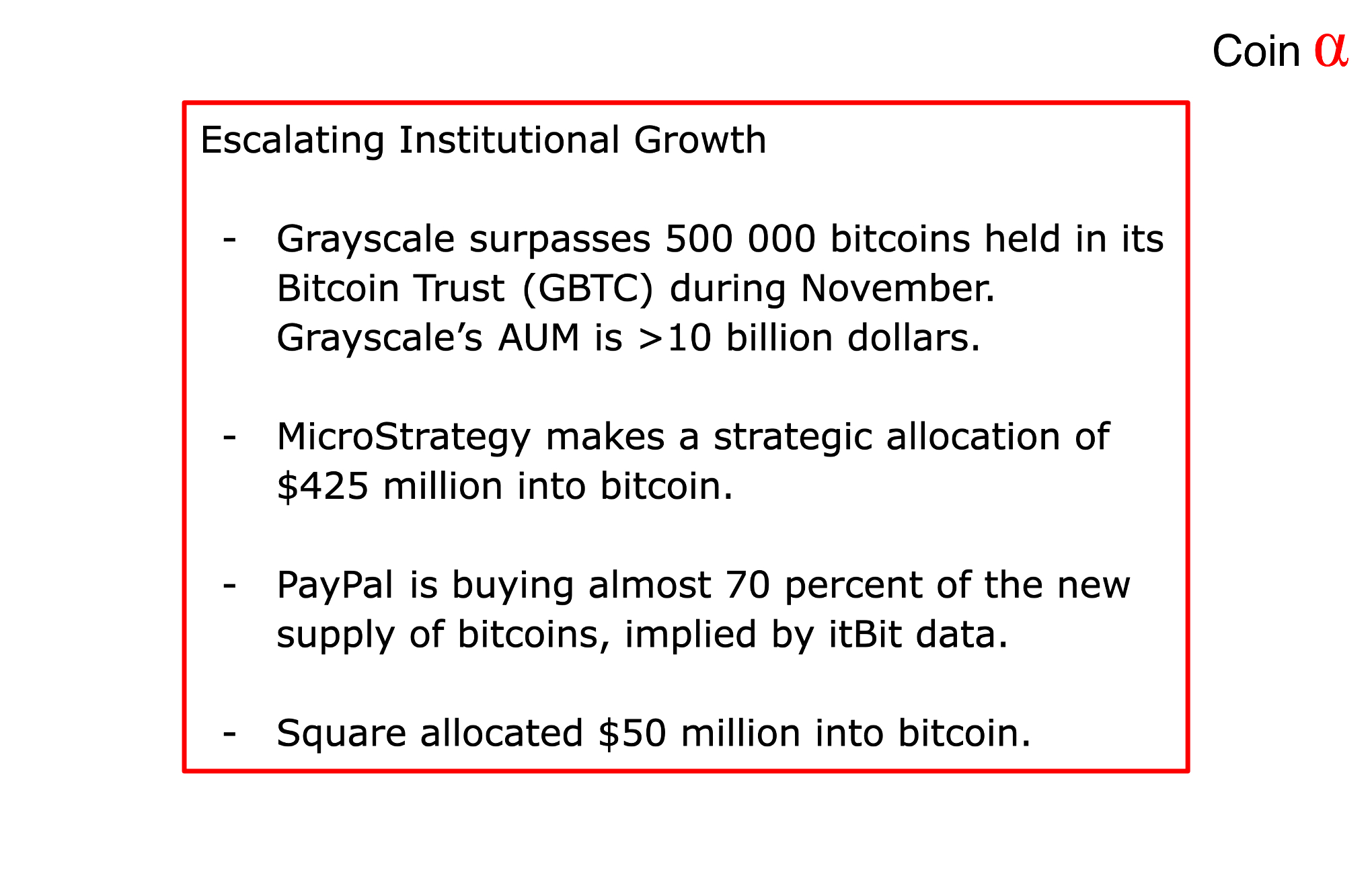

MicroStrategy’s allocation coincides with larger paradigm shift in institutional interest, Grayscale’s Bitcoin Trust GBTC surpassed 500 000 bitcoins in November. Grayscale is known to serve institutional clients, particularly hedge funds. PayPal is reportedly buying 70% of the new supply of bitcoins, possibly even creating a scenario for “bitcoin shortage”, as demand exceeds supply.

Do institutions know something we don’t? By buying bitcoin, institutions are most likely hedging the following events and scenarios:

Growing general uncertainty

Huge deficits

Modern Monetary Theory (MMT)

Possible Facebook Diem (Libra) launch in Q1 2020

Rising popularity of socialism

Unsustainable monetary policies

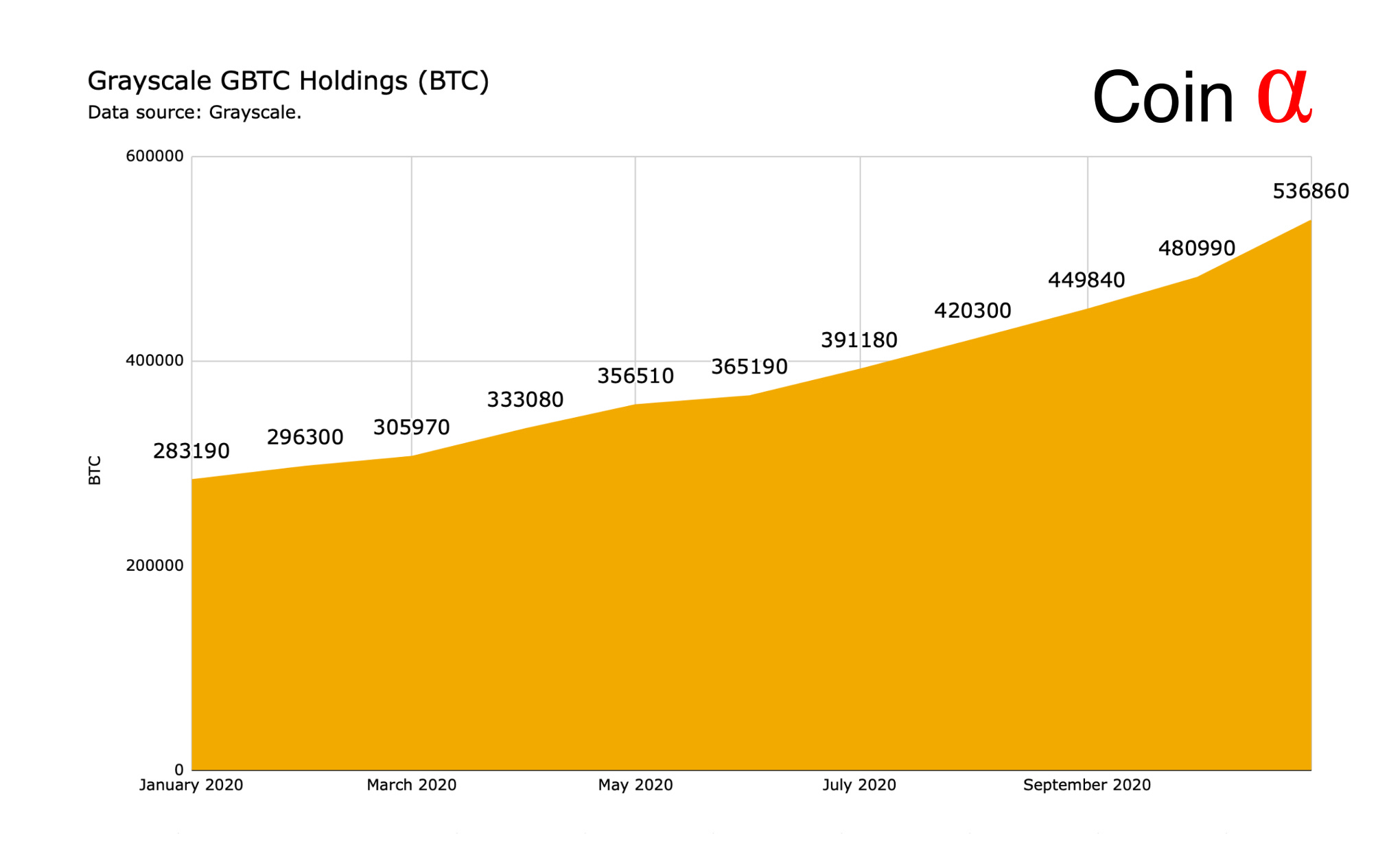

Grayscale Increases Institutional Holdings in GBTC, ETHE

Grayscale’s Bitcoin Trust (GBTC) is one of the most explicit indicators of growing institutional appetite. GBTC’s bitcoin (BTC) holdings have nearly doubled this year, rising from January 283190 bitcoins into 536860 in November. Institutional investors (hedge funds) represent 81 percent of Grayscale’s investor base, other notable segments being accredited individuals (8%), and family offices (8%).

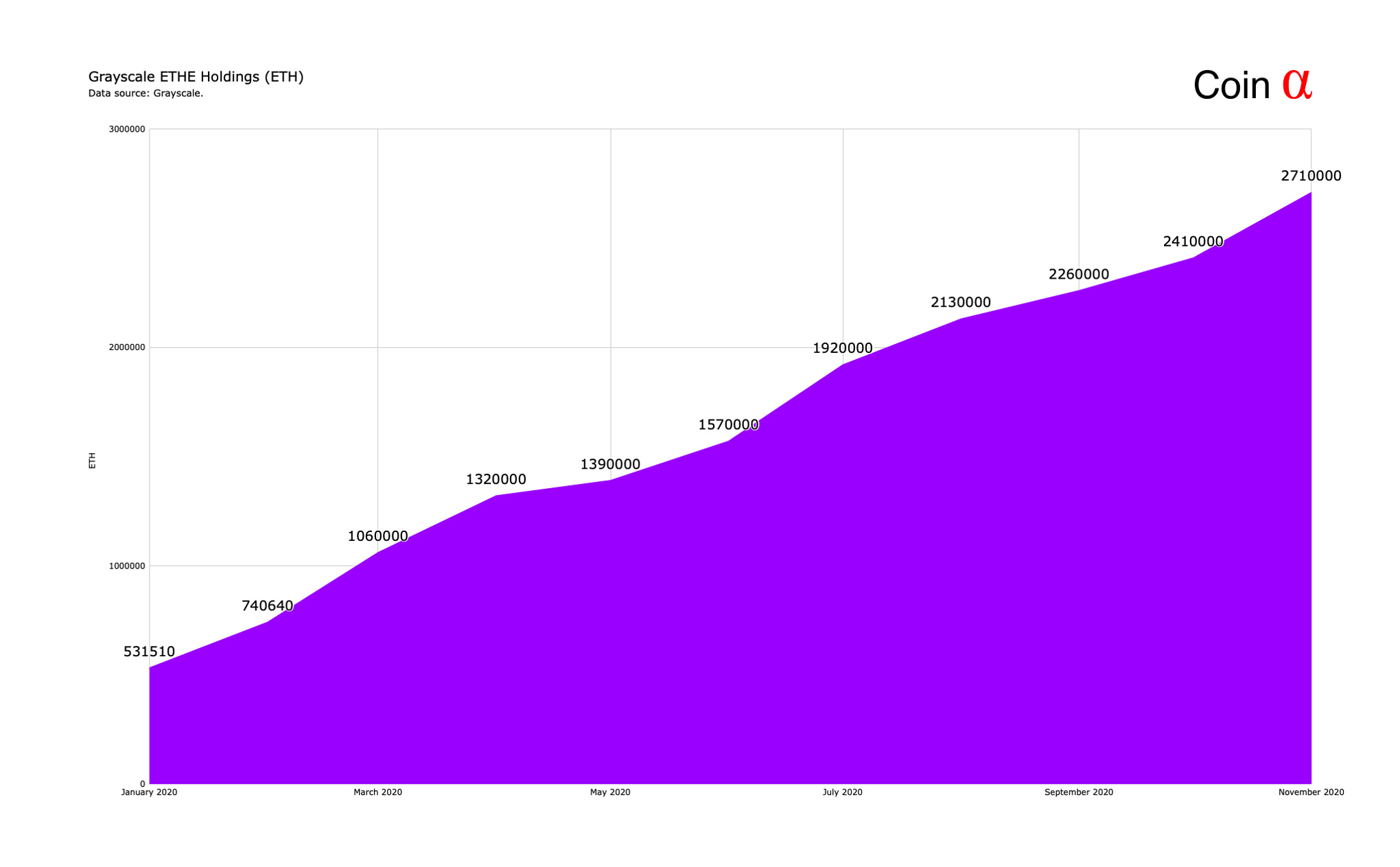

Grayscale’s Ethereum Trust (ETHE) has seen even more substantial growth, rising 490,90% in terms of Ethereum (ETH) holdings during this year. Grayscale’s total AUM is above 6 billion dollars.

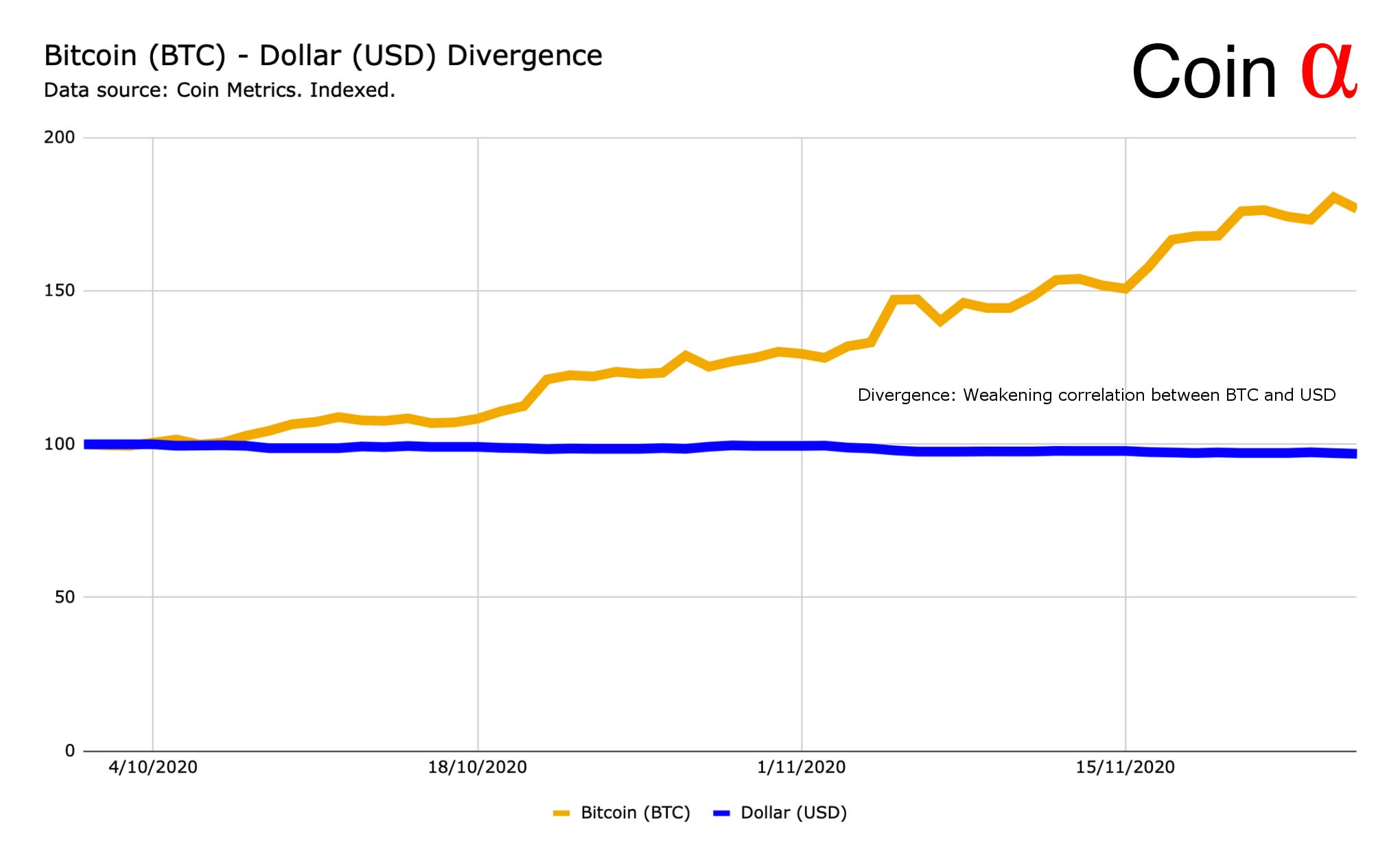

Bitcoin - Dollar Divergence

As forecasted in our previous November Outlook, Biden’s victory is expected to weaken the U.S. dollar. November and early December have proved this hypothesis to be true with USD clearly weakening against bitcoin (BTC) and euro (EUR). In general, weak dollar has historically been bullish to bitcoin and vice versa.

Libra Re-Launch in January?

The social media giant and technology company Facebook is reportedly planning a Libra relaunch during January 2021, the enterprise has been rebranded as Diem. The Libra Association now plans to launch a single dollar-backed coin. It would compete directly with other stablecoins, such as USDC, PAX and Tether (USDT). Facebook’s current user base is close to 3 billion, if they’re even able to convert 1-10% of their user base into the Diem ecosystem, it would create an enormous competition to traditional national currencies.

Comparing 2017 and 2020 Bull Market Characteristics

As bitcoin’s (BTC) price bounces around $20K level, it’s good to take a recap into last big bull market of 2017. When exploring the characteristics of 2017 it’s clear that the last cycle was heavily retail-driven. 2017 market was uplifted by ICO funding rounds, usually based on ERC-20 tokens. The new emerging token market also created a perfect environment for fraudulent actors, leading to highly speculative strategies and pump&dump schemes. 2017 also included high correlation between bitcoin and altcoins.

In a stark contrast to 2017, 2020 bull market has been mostly driven by institutional demand including companies like Grayscale, MicroStrategy, PayPal, and Square. While 2017 bull market was retail-biased, 2020 contains less retail participation. 2020 cycle has also been featured with less correlation between bitcoin and altcoins.

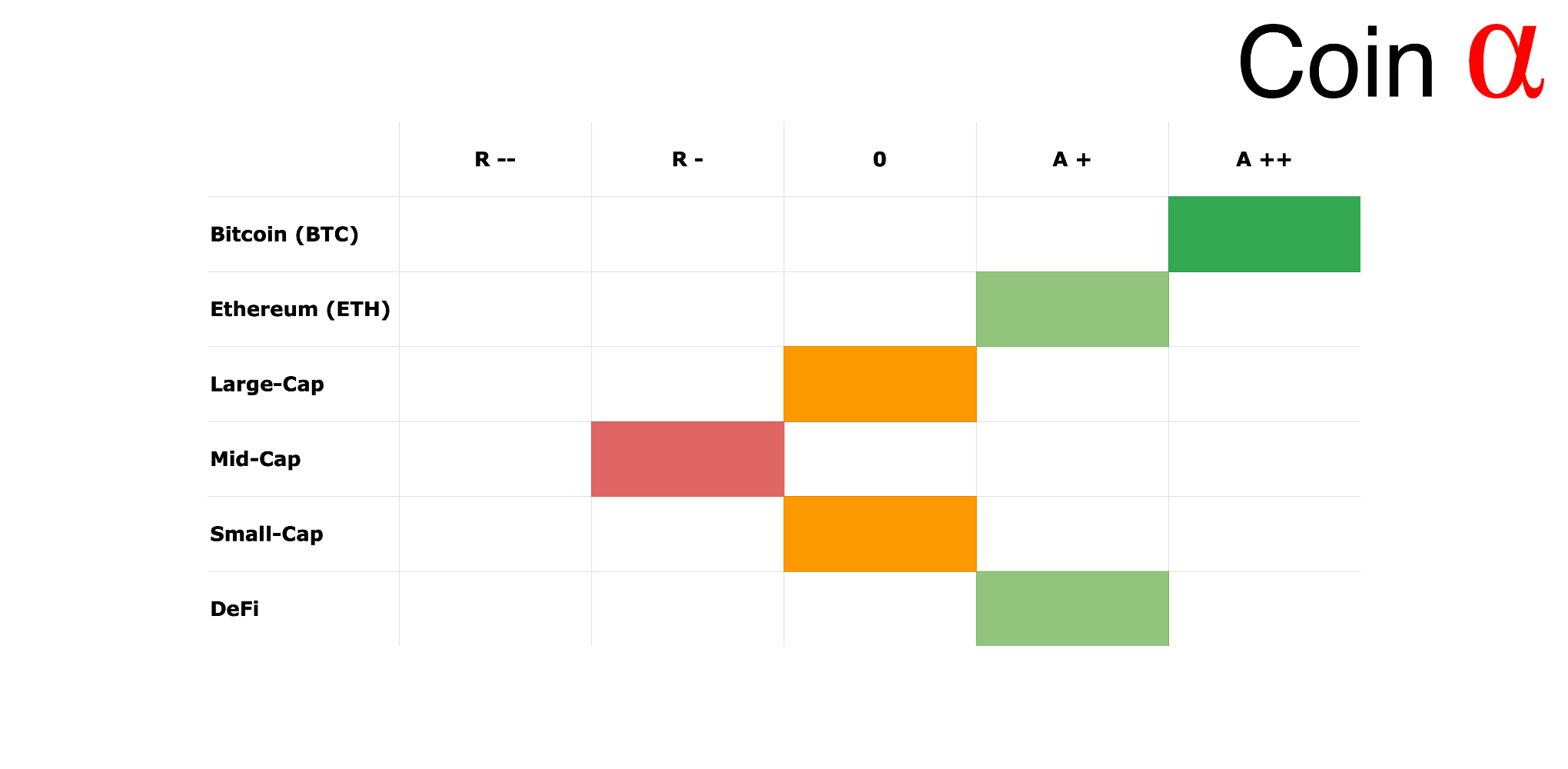

Allocation Model for Digital Assets

In this segment we maintain a model allocation for each month, consisting of most significant digital asset classes, including Bitcoin (BTC), Ethereum (ETH), Large-Cap, Mid-Cap, Small-Cap, and DeFi (Decentralized Finance). The assets are evaluated by placing them in following five categories:

A ++ (Accumulate)

A + (Slightly accumulate)

0 (Neutral)

R - (Slightly reduce)

R -- (Reduce)

Bitcoin (BTC) / A ++

Bitcoin (BTC) remains in the A ++ (accumulate) classification. Bitcoin’s investment horizon looks exceptionally promising with growing institutional appetite. Additionally the possible Libra launch next year would uplift the market.

Ethereum (ETH) / A +

Ethereum (ETH) stays in the A + ( slightly accumulate) segment. Ethereum is the main ecosystem and platform for future decentralized finance (DeFi) and decentralized applications (dapp). Ethereum’s future growth will be fueled by increasing amount of decentralized future products and services. By recent data, Ethereum seems to be increasingly correlated with Bitcoin.

Large-Cap / 0

Large-Cap digital assets, usually the top 10 cryptocurrencies, continue in the 0 (neutral) segment. The cryptocurrencies with large market caps are likely to be correlated with bitcoin, yet they might be eclipsed by dominant Bitcoin and Ethereum.

Mid-Cap / R -

Mid-Cap digital assets proceed in the slightly negative territory (R -). The Mid-Cap digital assets are usually projects with medium-sized market caps and cryptocurrencies in this segment are somewhat old. As they’re less known by retail, some of them might easily be replaced by other digital assets.

Small-Cap / 0

Small-Cap digital assets, usually the mass of cryptocurrencies with small market caps, continue in the neutral (0) category. Small-Caps are usually niche-class cryptocurrencies making them highly volatile. Small-Caps offer considerable upside for a veteran trader, but they might be notoriously illiquid.

DeFi / A +

DeFi, or Decentralized Finance, assets remain in the A + ( slightly accumulate) segment. DeFi platforms are quickly expanding in value and quantity, we expect DeFi to be one of the major drivers for cryptocurrency industry in upcoming years.

Want to Know More?

Subscribe to Coin Alpha’s future updates here on Substack.

Editor: Timo Oinonen. LinkedIn. Twitter.

Disclosure: The information provided is for informational purposes only and is subject to change without notice. The information presented in Coin Alpha should not be construed as investment advice.